Indian semiconductors: Now or never; It is time for the states to think big

India used to produce germanium semiconductors in the 1960s and could have been a leader in fabs. PSUs like BEL and HAL restricted themselves to defense and the 1989 devastating fire at the SCL complex at Chandigarh pushed India way behind in the semiconductor game.

Being a witness to failure in multiple attempts to get a semiconductor fab into India in the past two decades, it is heartening to see significant proactive efforts by the government in this direction today. There were times since 2005 when it looked certain, but delays and contradictions within the government led to efforts like Fab City and Intel Fab fizzling out. Intel then chose China and Vietnam over India due to the government’s delayed semiconductor policy. All subsequent efforts from 2007 onwards to bring AMD and Intel failed and endeavors with consortiums like Hindustan Semiconductor Manufacturing Corporation with ST Micro and Silterra Malaysia as well as Jaiprakash Associates with IBM and Tower Semiconductor also failed due to delayed decisions.

It is great to see major Indian businesses like Vedanta and Tata come out in this important and strategic market through their investments, an important component that was missing earlier. Vedanta’s commitment to constructing an integrated semiconductor and display fab in Gujarat is a testament to the strategic direction India can take riding on the strength of such home-grown partnerships.

Much like oil, semiconductors play a pivotal role in economies worldwide, and India’s focus on this sector is timely and crucial. The shifting dynamics and geopolitical threats to the global semiconductor supply chains require India to secure and engage in this space. India needs to act quickly, considering mature semiconductor markets are aggressively ramping up offers to established global players.

The US, Korea, Japan, Taiwan, and the European Union have significantly higher integrated industrial and university systems. There are also regional cooperation agreements like the “Three Amigos”—USA, Canada, and Mexico—with a keen focus on semiconductors. (Mexico makes a case for more localized semiconductor supply for America’s China+1 strategy.) The US has committed a substantial $52 billion in subsidies through the CHIPS and Science ACT and a 25% investment tax credit to attract new investments. The CHIPS Act allocates $10 billion specifically for expanding fab capacity in mainstream and mature nodes. The European Union has also approved a €43 billion incentive package.

South Korea has a $450 billion investment plan, with contributions from Samsung and SK Hynix, supported by tax incentives, lower interest rates, regulatory simplifications, and infrastructure enhancements from the government. Taiwan has also introduced rules allowing companies to convert 25% of their R&D expenditures into tax credits. Japan is actively pursuing international partnerships and providing subsidies to encourage collaborations with Japanese chip manufacturers.

China, due to tightening US export controls and changes in the global supply chain has doubled its decade-long, $150 billion Big Fund semiconductor subsidy program and has made significant progress in expanding chip capacity, holding over 17% of total global chip production, predominantly in mature technology nodes. China is also strategically reducing its reliance on the global industry, particularly in advanced technology nodes.

Back home, states like Gujarat are leading the way having offering 40% additional capital assistance over the central government incentives. They provide a 75% subsidy on the first 200 acres of land for fabs and further land at a 50% subsidy. Uninterrupted water supply at a subsidized rate of Rs 12 per cubic meter for five years and electricity tariff supports for a power rate of `2 per unit for a decade are other attractive incentives offered. States like Orissa and Uttar Pradesh have also announced their semiconductor policies and are following suit.

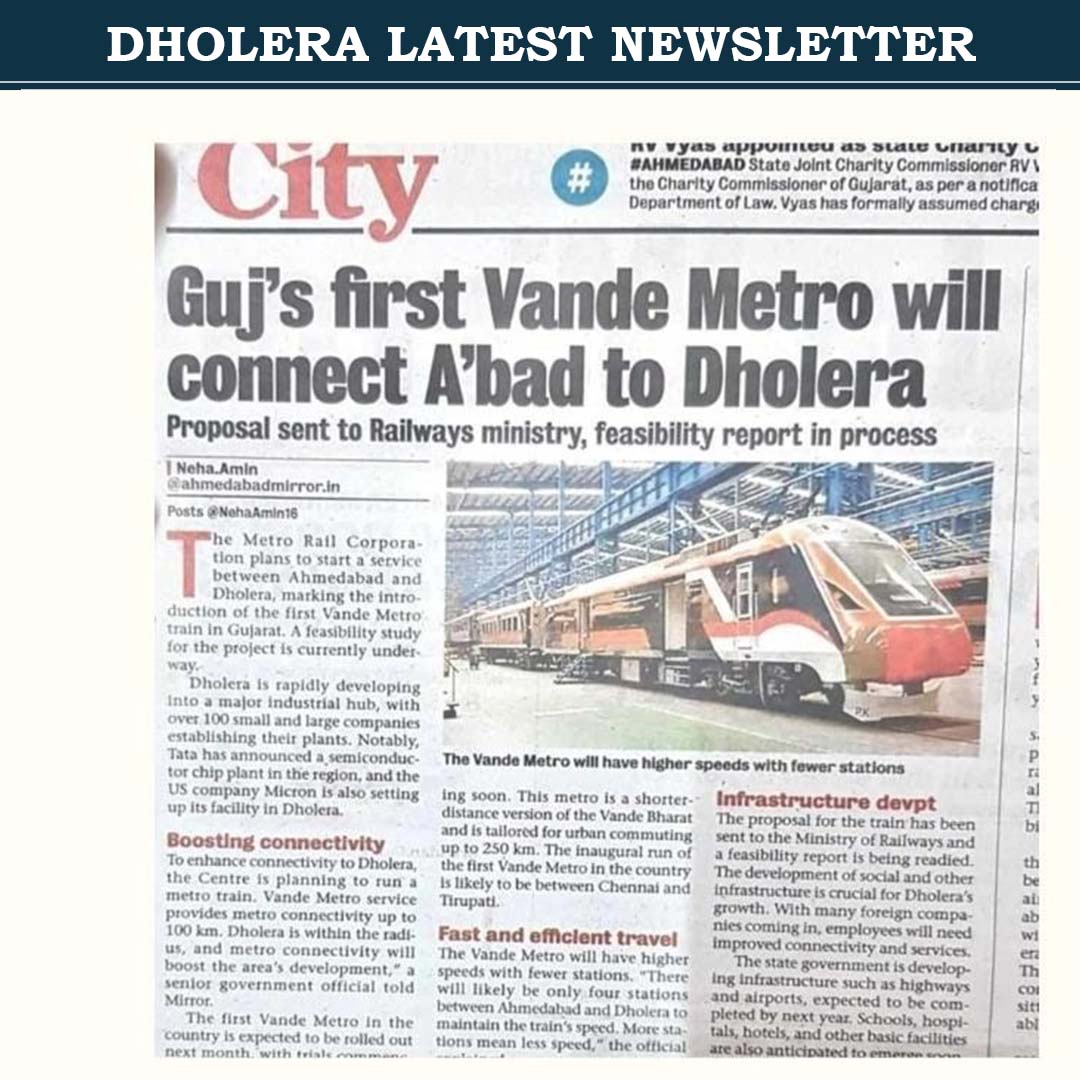

For the past year, Gujarat has attracted significant interest from potential investors with Micron Technology committing a $2.75 billion investment for its assembly, testing, marking, and packaging (ATMP) facility. Vedanta’s MoU with the Gujarat government is a critical piece in the electronics supply chain since it also covers display. Vedanta is aiming to construct an integrated semiconductor and display fab in Dholera’s Smart City and Special Investment Region (SIR).

Gujarat leveraging its existing appeal—from investor-friendly policies, transparency, and efficient decision-making—has an advantage. The state, through Gujarat State Electronics Mission (GSEM), is offering its robust infrastructure, abundant power, access to water, a vast coastline, and industry-friendly image and can become a prime destination for semiconductor and electronics manufacturing projects.

India’s past failures hinge on additional factors, beyond the proactiveness of states. Establishing successful semiconductor ventures requires strategic partnerships between global technology experts, equipment suppliers, and importantly large Indian businesses like the Tatas and Vedantas, who may understand India better.

India’s entry into the semiconductor manufacturing arena is indeed a “now or never” opportunity. India has great human capabilities already in semiconductor design, as almost every semiconductor major has an Indian presence in the design of the most advanced chips. It is time for India to leverage this and have a collaborative effort between the government, Indian industry, and global tech players to go for the fab. It is also time for Indian states to think big and compete with rival geographies rather than neighboring states.

Rameesh Kailasam & Dhiraj Gyani, respectively, CEO, and senior director (policy & operations), IndiaTech.org